The global picture

PwC's Net Zero Economy Index tracks the progress G20 countries, which produce around 80% of global emissions, have made to reduce energy-related CO2 emissions and decarbonise their economies.

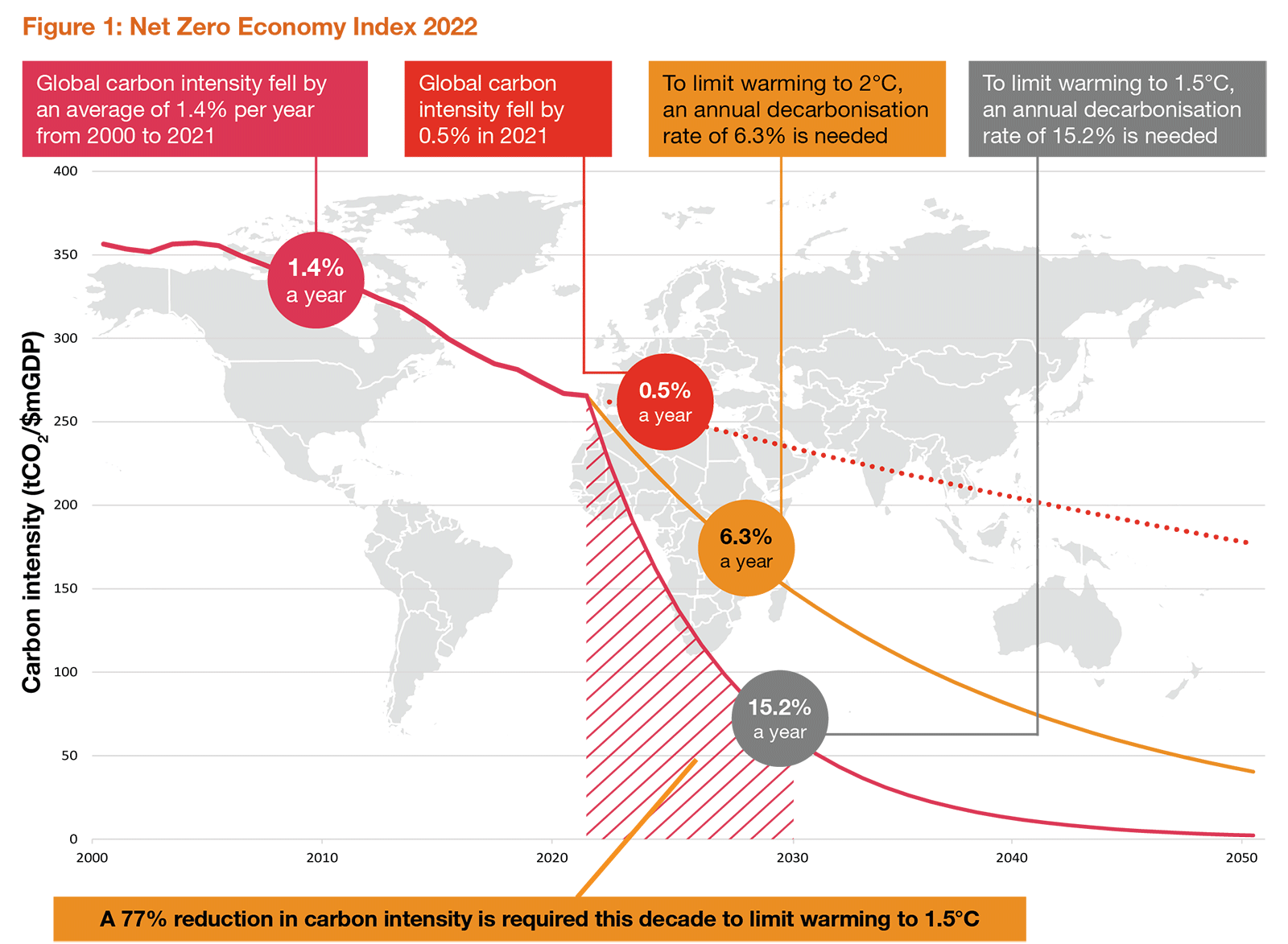

Seven years on from the groundbreaking Paris Agreement, our analysis shows that the world is continuing to move further from the rate of decarbonisation required to limit warming to 1.5°C above pre-industrial levels. In 2021, the global decarbonisation rate fell to its lowest level in over a decade at just 0.5%, well below the average of 1.4% per year achieved between 2000 and 2021, and far below the rates of decarbonisation required to limit warming to 1.5ºC. When compared to 2020 levels, global energy consumption and energy related emissions increased by 5.5% in 2021. Absolute levels of carbon intensity vary across the G20, as nations are at different stages of development and have very different socio-economic bases. In 2021, 266 tonnes of CO2 was emitted for every million dollars of GDP generated worldwide, ranging from an average of 189 tonnes in the G7 to 351 tonnes in the E7 (Emerging Seven).

Only 11 of the G20 managed to reduce their carbon intensity in 2021, compared to 16 of the G20 achieving a reduction in carbon intensity by reference to their pre-pandemic 2019 levels. Looking closer at how some of the world's leading economies performed in terms of decarbonisation in 2021, the US (0.1%), India (2.9%), Japan (0.6%), Germany (1.7%) and France (1.4%) all saw increases. The best-performing country was South Africa (-4.6%), ahead of Australia (-3.3%), China (-2.8%), Turkey (-2.7%) and Canada (-2.2%).

The lifting of pandemic restrictions in 2021 gave way to a much needed resurgence in economic activity, but with this, there has been a rebound in emissions. The 2021 data appears to show that the recovery from the COVID-19 pandemic has not—at least in the short-term—been a green one.

When the COVID-19 variance is removed from the data and we compare 2021 levels with pre-pandemic levels in 2019, we see a global decarbonisation rate of 3%. This suggests that, while decarbonisation has occurred over this period, there's still a long way to go. Removing noise from the data in this manner allows for a more accurate reflection of decarbonisation progress.

Although we see increasing levels of policy, business and investor commitments, real progress on decarbonisation is slow and does not yet create the confidence that promises made will be delivered. There is no single pathway to net zero with each country moving at a different pace and by different means. Ultimately, however, all nations must accelerate action with an urgent need to reduce global carbon intensity by 77% by 2030.

Menu